Dreaming of owning your own home? It’s an exciting journey, but one that requires careful planning and preparation. To purchase a house with a mortgage, you’ll need a deposit, proof of income, a good credit score, and pre-approval for a mortgage.

Before you start house hunting, it’s crucial to assess your financial situation. Take a close look at your savings, income, and current debts. This will help you determine how much you can afford to spend on a home and what type of mortgage you might qualify for before falling head over heels for a property currently on the market.

Don’t forget about the additional costs that come with buying a property either. You’ll need to budget for solicitor fees, in-depth housing surveys, stamp duty, and potential home repairs or renovations. Being prepared for these expenses will make your home-buying experience much smoother and stress free.

The Home-Buying Process

Purchasing a home involves several key steps and considerations. You’ll need to evaluate your finances, choose a suitable location, assess whether you are eligible for any purchasing schemes, and decide on the type of property that best fits your needs and lifestyle.

Assessing Your Budget

Start by reviewing your income, expenses, debts and savings. Calculate how much you can comfortably afford for a deposit and monthly mortgage payments. Don’t forget to factor in additional costs like property taxes, insurance, and general maintenance to avoid a shock later down the line.

Consider getting pre-approved for a mortgage. This will give you a clear idea of your budget and make you a more attractive buyer to available property sellers.

Remember to leave some wiggle room in your budget for any unexpected expenses. It’s wise to have an emergency fund set aside for home repairs, such as a new boiler, or other unforeseen costs that may spring up.

Choosing the Right Location

Think about your daily routines and priorities when selecting a location. Consider factors such as:

- Commute times to work

- Proximity to schools, shops, and amenities

- Crime rates and safety

- Future development plans for the area

Research property values and trends in different neighbourhoods that meet your needs. This can help you identify areas with good potential for appreciation to ensure you are making a good investment.

Visit potential locations at different times of day to get a feel for the community and any potential issues like noise & light pollution, or congested traffic.

Deciding on Property Type

Reflect on your lifestyle and long-term plans when choosing a property type. Do you need a spacious garden for pets or children? Or, would you prefer a low-maintenance flat?

When considering your options, these are often the most popular choices:

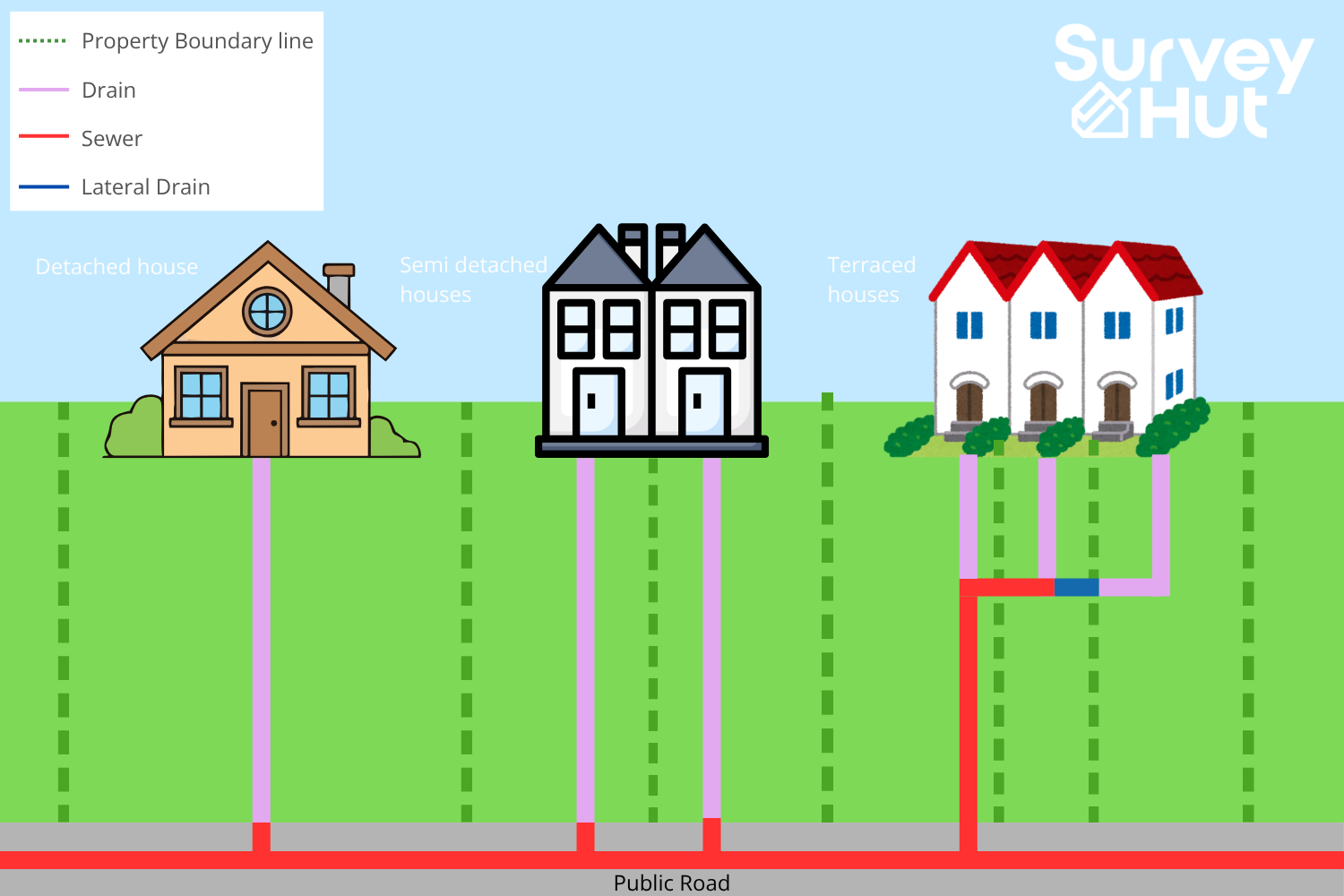

- Detached houses

- Semi-detached homes

- Terraced houses

- Flats or apartments

You should also take some time to think about the age of the property and its current condition. Newer homes might require less maintenance, while older properties could offer more character but need much more upkeep and may require future repairs. These could add value to your property and accommodate changing needs over time, but could create unexpected future costs to plan for.

It’s always a good idea to commission a suitable home survey to ensure peace of mind when looking to buy your perfect home.

Financial Considerations

Purchasing a house involves careful financial planning and preparation. You’ll need to consider several key monetary aspects to ensure a smooth and successful home-buying process.

Saving for a Deposit

Start by setting a savings goal for your deposit. Most lenders require at least 5-20% of the property’s value as a down payment. The larger your deposit, the better mortgage rates you’re likely to secure.

Create a dedicated savings account for your house fund to keep it separate and away from temptation (of spending it on holidays, for example). Setting up automatic transfers to this account each payday and looking for high-interest savings accounts to maximise your returns can be an elegant solution to saving for this deposit.

Exploring Mortgage Options

Research different mortgage types to find the best fit for your situation. Fixed-rate mortgages offer stability with consistent monthly payments, while variable-rate mortgages might provide lower initial rates.

Compare offers from multiple lenders, including banks, building societies, and mortgage brokers. Look at interest rates, fees, and loan terms. Check your credit score and work on improving it if needed. A higher credit score can lead to better mortgage terms and reduced rates.

Consider seeking professional advice from a mortgage advisor to help you navigate the complexities of home loans.

Budgeting for Additional Property Costs

When purchasing a property, factor in other expenses beyond the property’s price itself. Stamp duty land tax can be a significant expense, varying based on the property value and your buyer status.

Budget for conveyancing fees, which cover legal costs associated with property transfer. These typically range from £850 to £1,500.

Set aside funds for in depth surveys and valuations. At Survey Hut, a basic survey costs around £425, while a comprehensive survey costs £625 or more. Despite the upfront cost of a home survey, they ensure peace of mind by identifying deadly defects, and offer opportunities for further negotiation on house price.

Don’t forget ongoing costs like insurance, council tax, and utility bills. These will impact your monthly budget as a whole upon moving in.

Legal Requirements

Purchasing a house involves several legal steps and requirements. You’ll need to navigate these processes carefully to ensure a smooth transaction and protect your interests.

Understanding Stamp Duty

Stamp Duty Land Tax (SDLT) is a tax you pay when buying property or land in England and Northern Ireland. The amount varies based on the property’s value and whether you’re a first-time buyer.

For properties up to £250,000, first-time buyers don’t actually pay SDLT. Above this threshold, however, rates increase progressively. If you’re not a first-time buyer, SDLT starts at 2% for properties over £125,000.

Buy-to-let properties and second homes incur an additional 3% surcharge on top of standard rates. It’s crucial to factor these costs into your budget when planning your purchase.

Conveyancing Process

Conveyancing is the legal transfer of property ownership from seller to buyer. You’ll need a solicitor or licensed conveyancer to handle this process.

Your conveyancer will conduct property searches, review contracts, and liaise with the seller’s solicitor. They’ll also manage the exchange of contracts and completion day arrangements for you.

Key legal steps include:

- Property searches

- Reviewing the draft contract

- Raising enquiries with the seller

- Agreeing on a completion date

- Exchanging contracts

- Transferring funds and completing the purchase

It’s vital to choose a reputable conveyancer to ensure all legal aspects are properly addressed. This helps protect you from potential issues that could arise after the purchase is complete.

Making an Offer and Closing the Sale

Once you’ve found your ideal home, it’s time to make an offer and finalise the purchase. This process involves several key steps to ensure a smooth transaction.

Preparing Your Offer

Crafting a compelling offer is crucial. Research recent sales of similar properties in the area to determine a fair price, considering the property’s condition and any repairs needed.

Decide on your maximum budget and initial offer amount in advance. Include any conditions in your offer, such as it being subject to a complete housing survey or mortgage approval. Your estate agent can help you draft the offer letter if need be.

The seller may counteroffer. Be prepared to negotiate, but stick to your budget. Once both parties agree, you’ll need to put down a deposit to secure the property and proceed with the next stages of completing the acquisition.

Property Survey and Valuation

A thorough survey is essential to uncover any potential issues with the property. At Survey Hut, we offer a range of surveys to suit your needs when establishing a property’s value and specifications. RICS Level 2 Surveys provide a more basic outlook, whilst our above-and-beyond Level 3 MAX Surveys provide extra reassurance about the condition of services such as electricity, gas and heating.

Our surveyors inspect the property and provide a highly detailed report. This document highlights any defects, necessary repairs, and potential problems.

At Survey Hut, we can also conduct a valuation to ensure the property is worth the agreed price. If issues arise, you may need to renegotiate the price or ask the seller to fix problems before proceeding.

Finalising the Sale

Once surveys and valuations are complete, it’s time to exchange contracts. Your solicitor will handle this process, ensuring all legal requirements are met.

You’ll need to arrange insurance from the exchange date. Finalise your mortgage and transfer the deposit to your solicitor.

On completion day, your solicitor will transfer the remaining funds to the seller’s solicitor. You’ll receive the keys and officially become the property owner.

Don’t forget to inform utility companies and update your address with relevant organisations!

Get in touch with Survey Hut today for a comprehensive Home Survey. We are held to the highest professional standards by the RICS, so you know that you’ll get a high-quality report. Make sure your perfect home, is perfect.

Sharing is caring!